Date: February 2026 (data through Jan 2026 for LA County; mortgage rates through Feb 19, 2026)

The big question: are we heading into a “good” market or a “bad” market?

For most buyers and sellers, 2026 is shaping up as a more balanced, rate-driven market—not the frenzy of 2021–2022, and not a crash scenario either. Small moves in mortgage rates have an outsized impact on affordability, buyer demand, and how quickly homes sell.

Where mortgage rates are right now

Freddie Mac’s Primary Mortgage Market Survey shows the 30-year fixed mortgage rate at 6.01% (Feb 19, 2026), down from 6.85% a year earlier—a meaningful improvement in affordability, even if rates are still elevated compared to the ultra-low era. (Freddie Mac)

Why this matters: In a market like Los Angeles, affordability is the gatekeeper. When rates drift down, buyer traffic tends to return quickly; when rates rise, demand cools quickly.

What the LA County data is signaling (right now)

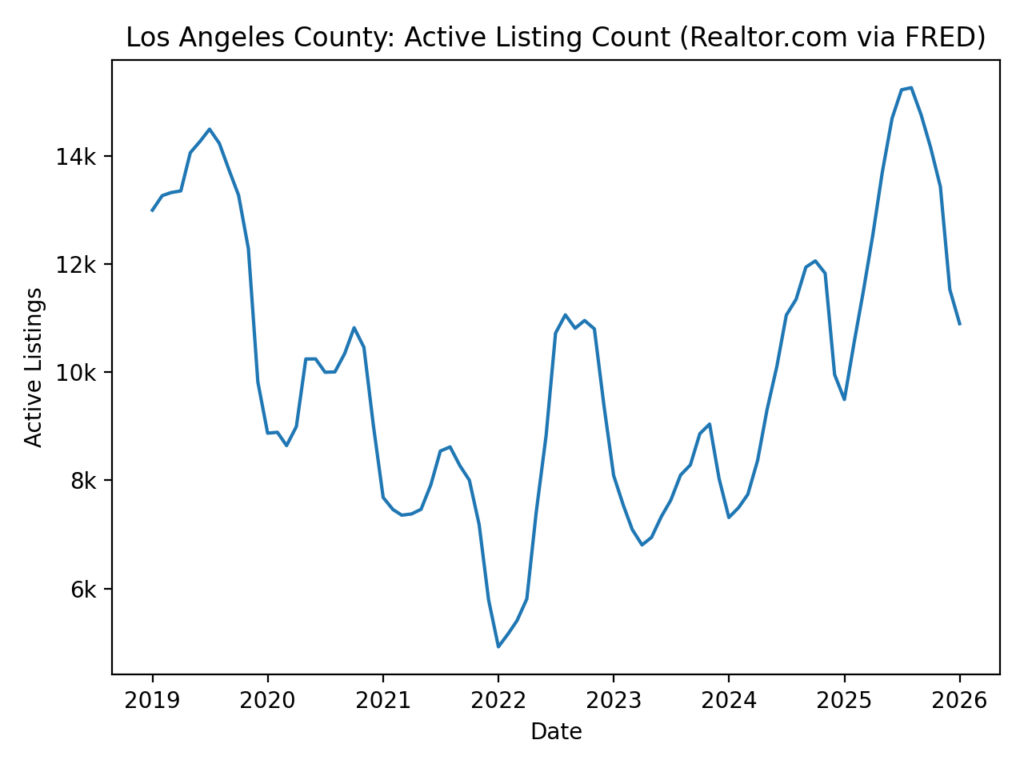

Using Realtor.com’s LA County market metrics (via FRED), here’s what stands out:

- More inventory (more choices for buyers): LA County had 10,896 active listings in Jan 2026, up about +14.8% year-over-year. (FRED)

Context: active listings were as low as 4,923 in Jan 2022, meaning today’s inventory is more than 2× that low point. (FRED)

- Prices are more selective: LA County median listing price was $950,000 in Jan 2026, about -4.2% year-over-year. (FRED)

Context: this listing-price series peaked around $1,132,472 (May 2024) and is down roughly ~16% from that peak, reflecting a market that’s become more rate-sensitive and more price-disciplined. (FRED)

- Homes are taking longer to sell: Median days on market reached 68 days in Jan 2026 (seasonality matters—January is often slower), and it’s higher than the ultra-tight period in 2022 when the series bottomed near ~29.5 days (May 2022). (FRED)

Translation: negotiation power has improved versus the most competitive years, especially on homes that are overpriced or need work.

So what should clients expect through 2026?

The most honest answer is: the market will likely follow rates. But there’s a practical “base case” many forecasters have been leaning toward:

- The California Association of REALTORS® 2026 forecast projects average 30-year fixed mortgage rates around ~6.0% in 2026 and a +3.6% increase in the CA median home price (to $905,000). (California Association of Realtors)

- Fannie Mae’s ESR outlook (Sept 2025) forecasted mortgage rates ending 2026 around ~5.9%, with housing activity improving into 2026. (Fannie Mae)

What that means in plain English for LA clients:

- If rates trend down, demand typically strengthens, and well-located, turnkey homes can return to faster timelines (and sometimes multiple offers).

- If rates hold around ~6%, expect a more normal market: homes can sell well, but pricing and preparation matter more.

- If rates move higher again, expect longer market times and more concessions, especially on homes that are dated, overpriced, or in less competitive micro-markets.

Buyer playbook for 2026

- Think in monthly payment, not just price. If the payment works today and the home fits long-term, waiting for a “perfect” rate can backfire if competition returns.

- Target negotiating leverage: longer days-on-market listings, properties with price reductions, or homes needing cosmetic updates.

- Use credits strategically: seller credits (and sometimes temporary buydowns) can be powerful tools when rates are still in the ~6% range—always review structure and timelines carefully.

Seller playbook for 2026

- Price-to-market wins. The market is less forgiving of aspirational pricing when buyers have more options.

- Condition and presentation matter more. Pre-inspection, clean disclosures, and strong curb appeal are higher ROI when the market isn’t hyper-competitive.

- Expect negotiation. With inventory higher than the 2022 lows, many buyers will ask for repairs, credits, or concessions—especially if a home has been sitting.

Bottom line

2026 looks like a good market for prepared sellers and a better market for buyers than the “anything goes” years—but the speed of the market will still be rate-driven. The best strategy is to base decisions on monthly affordability, local neighborhood inventory, and property-specific competitiveness—not headlines.